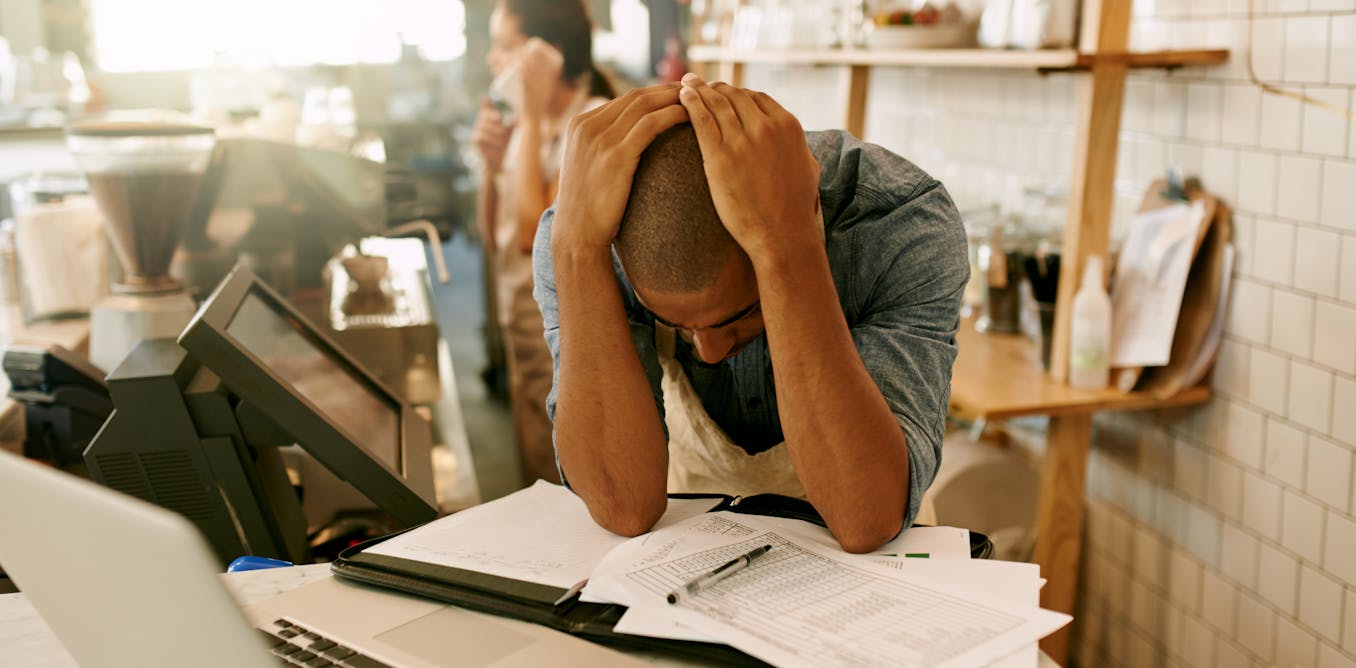

WITH rising costs and rushes in consumer spendingsmall businesses have been struggling recently.

Continued economic pressures cause significant stress and burnout amongst small business owners, while confidence continues to say no.

Data from the Ministry of Business, Innovation and Employment shows the corporate the variety of liquidations increased by 40% in the primary eight months of 2024 in comparison with 2023 Construction, retail and hotel industry have been hit hard by rising costs and falling spending.

The economic climate has been in comparison with following the 2008 global financial crisis (GFK). This time, nevertheless, the issues of small and medium-sized enterprises may be more serious.

New Zealand in the course of the 2008 crisis

GFC, rooted in excessive taking risks in credit markets in the United States, Ireland and elsewhere, was one of the serious economic shocks in the post-war period.

Globally, central banks I quickly lowered my interest rates of interest to encourage lending. By rate of interest cuts governments encouraged consumers to spend money to get out of the crisis.

New Zealand official money rate dropped sharply from 8.25% in July 2008 to 2.5% in May 2009. Falling rates of interest have benefited many mortgage holders.

The the federal government has also moved forward capital spending, encouraged investment and provided support for small businesses.

At the identical time, China had growth spurt and developed an appetite for New Zealand agricultural exports. Trade between each countries almost 3 times between 2007 and 2016.

These conditions place our performance in terms of gross domestic product per capita amongst preferably in the OECD. In the present crisis, we’re among the many worst.

Holding the belt tightly

This time it’s different. New Zealand is trying to avoid wasting itself from economic problems. High inflation and subsequently higher rates of interest have forced many New Zealanders to tighten your seatbelts.

According to one studyAustralian and New Zealand consumers reduced their spending at small and medium-sized businesses by 60% – essentially the most of any region surveyed.

The government also radically reduced spending and made hundreds of public sector staff laid off. Further rate of interest cuts may be on the horizon to assist achieve inflation neutrality tax relief.

While all small businesses are facing the identical storm, they will not be in the identical boat.

Some, corresponding to technology firmsor in specific locations corresponding to construction firms in Southare still in demand. There have also been changes in consumption city centers to suburbs, shopping malls and online.

But for others, the upkeep cost crisis has forced customers to repair quite than replace takeaway meal as a substitute of eating in a restaurant and going to bargain hunting on the Internet, quit the gym or do more DIY.

In fact, credit reference agency Centrix found that it currently stands at 461,000 consumers in New Zealand is in arrears with repayments. Savings measures for consumers have hit many retailers in addition to small service firms.

Foreign gueststhat typically spend in these categories are also still below pre-pandemic levels. Customer spending is restricted.

Small businesses are experiencing a “cost of doing business” crisis. Costs increased rapidly. Wages, materials, rents and the price of capital increased. Further compliance costs and lack of infrastructure stretch business budgets.

However, passing on the rise to customers is usually inconceivable given the constraints of shrinking discretionary purchasing power. In short, less purchasing power and rising costs for a lot of small businesses mean the candle is burning at each ends.

Too expensive to shut

The seriousness of the situation is unlikely to be fully reflected business closure statistics. Small businesses do every thing to survive. People are working longer hours and cutting back on the cash they take out of the business to administer money flow.

Leaving the workforce can be difficult in a good labor market – in part because fewer positions can be found for the growing variety of job seekers.

Business loans are frequently secured against family home or by personal guaranteewhich suggests business liquidation is the worst case scenario and relatively rare.

Instead, small businesses do every thing they can to increase their runway to avoid legal liquidation. They are likely to close quietly if they run out of options.

However, rising rates of interest have increased exposure. And as home values decline, small businesses are less capable of leverage the family home for extra financing.

These processes worked in the other way in the course of the 2008 crisis, when initially shrinking demand was accompanied by a decline in the price of credit. Simply put, gasoline has been added to the tank.

Interest rates to the rescue?

There is hope. The recent reduction in rates of interest has improved economic sentiment, and business confidence has reached approx the best in ten years in September.

On the eve of it “no frills” budget.Finance Minister Nicola Willis warned of inauspicious times before the economic situation improves.

Global declines in rates of interest mean Willis’ predicted rise has begun, however the final result is just not guaranteed.

There were consumers pessimistic on the New Zealand economy for over two years, a stark contrast to the GFC where their confidence grew rapidly.

Demand from Chinakey New Zealand market, faces its own economic challenges.

Government narrative shapes conditions for the economy. Yes, we’d like to ‘stand by the books’, but this must be balanced with encouraging small business and innovation.

Like others small economiesNew Zealand needs a sustained commitment to infrastructure and exports, in addition to investment in science and innovation to support the small business sector.

The government must provide small businesses with the arrogance to thrive and forestall long-term recovery from the economic downturn.