Health and Wellness

How to remove unpaid medical accounts from credit reports can help consumers

New York (AP) – lenders will not give you the chance to consider unpaid medical accounts for a credit history factor once they assess potential borrowers within the US for mortgage loans, automotive loans or business loans, in accordance with the principle Consumer Fundamental Protection Office finalized on Tuesday.

Removal of medical debts from consumer credit reports It is anticipated to increase the credit results of thousands and thousands of families by a mean of 20 points, said the office. CFPB claims that his research has shown that outstanding claims regarding healthcare are a weak predictor of somebody’s ability to repay the loan However, they are sometimes used to refuse to have a mortgage application.

Three national credit reporting agencies – Experian, Equifax and Transunion – said last yr that they remove medical collections below USD 500 from American consumer loans reports. The recent principle of presidency agency goes further, prohibiting all in arrears to medical accounts appearing in credit reports and prohibiting lenders to use this information.

The principle enters into force 60 days after publication within the federal register, although President Elek Donald Trump proposed broad changes and limitations of the CFPB regulatory range.

Here’s what to know:

How many individuals will affect it?

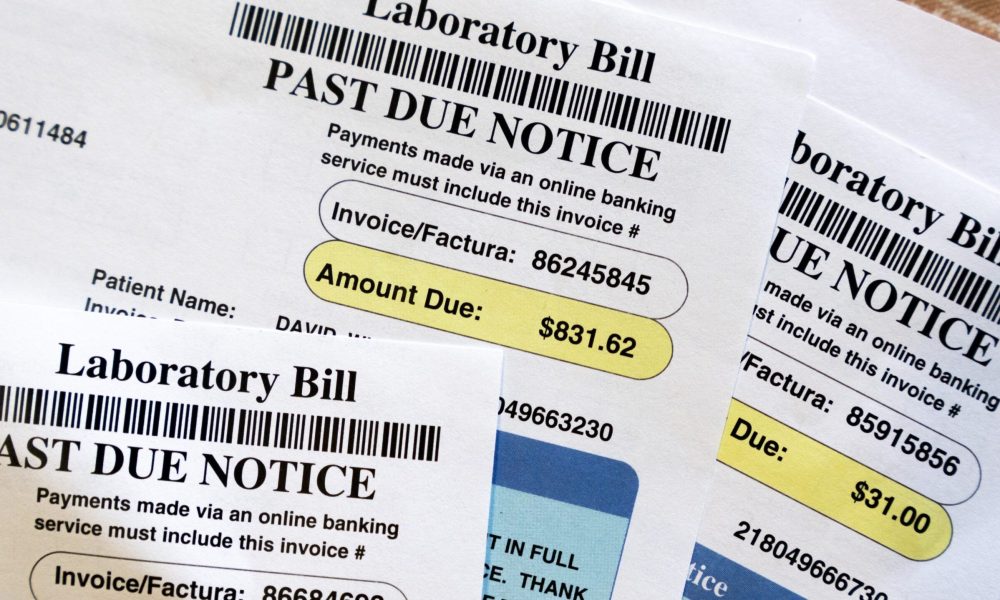

CFPB estimates that the principle will remove $ 49 million in medical debt from credit reports of 15 million Americans. According to the agency, one in five Americans has at the very least one debt collection account by way of their credit reports, and greater than half of the gathering entries in credit reports concerns medical debts.

The problem disproportionately affects colourful people, said CFPB: 28% black and 22% Latinos within the US carries medical debt compared to 17% of white people. While national credit reporting agencies have voluntarily agreed to ignore medical debt below USD 500, many consumers are much higher than this threshold of their reports.

What will likely be the impact of consumers?

CFPB claims that its operation will provide thousands and thousands of consumers to increase access to loans and can lead to approval of about 22,000 additional mortgages a yr. According to the office, Americans with outstanding medical accounts can make their credit results increase by 20 points on average.

The rule was also developed to increase the protection of privacy and help collectors of debts before using the credit reporting system to force people to pay bills that it shouldn’t be to blame. CFPB has found that consumers often receive inaccurate bills or asked to pay bills that ought to be covered by insurance programs or financial assistance.

Moreover, lenders will likely be excluded to use information on medical devices, similar to prosthetic limbs, in order that they serve them as a loan collateral and acquiring acquisitions, in accordance with the CFPB announcement.

How do supporters react?

Non -profit organizations within the healthcare space are satisfied.

“This decision is great news for everyday Americans,” said Carrie Joy Grimes, the founding father of the Personal Workmoney finance organization. “Medical debt is not a reflection of bad with money – each of us can experience illness or injuries. Thanks to this new principle, Americans will now be able to focus less on the load on medical debt, and more on returning to their feet. “

Patricia Kelmar, director of the Health Care Campaign on the American group of research on public interest, said that the rule would help “many financially responsible families who have accumulated medical debt from unpredictable health problems, high costs from their own pocket, denying insurance claims and errors settlement. “

What must you do after receiving the high medical account unexpectedly?

One sec High medical accounts are common within the USAIn this for natural individuals and households with insurance, there are relief.

First, determine whether you qualify for charity. Federal law requires non -profit from reducing or write off accounts for people depending on household income. To determine in case you qualify, seek for the Internet to hospital or healthcare with the phrase “charity care” or “financial assistance policy”. Dollar of the Non -Profit organization also ensures Simplified online tool for patients.

Then the appeal based on the provisions of the NO Surpises Act, the Federal Act, which claims that insurance firms must correctly cover all services outside the network related to the emergency and certain medical care not related to independence. If you might be charged greater than you might be used to or expect whenever you receive services online, this account could also be illegal.

In addition: all the time ask for a special bill. Medical interaction is notoriously complicated and filled with mistakes. A special bill is included within the settlement codes of all received care. If something is between these codes and care, questioning the bill can bring changes.

Another approach – a comparison of the account with the estimates of insurance firms regarding a good service fee can also help. If the worth you downloaded is greater than the common, you can reduce costs. You can even take the supplier to court in small claims in reference to the divergence – or inform him concerning the case.

Finally, all the time compare the “explanation of benefits” of the insurance company with the bill. The hospital act must correspond to the reason of the prices which might be covered and never covered. If this shouldn’t be the case, you will have a unique reason not to pay and ask the supplier for further work with the insurance company.

Even after taking these steps, you can all the time appeal against health claims in an insurance company, in case you think there may be any reason why the accounts ought to be completely or greater than the corporate initially decided. You can also contact your insurance commissioner for support.

(Tagstranslat) medical debt